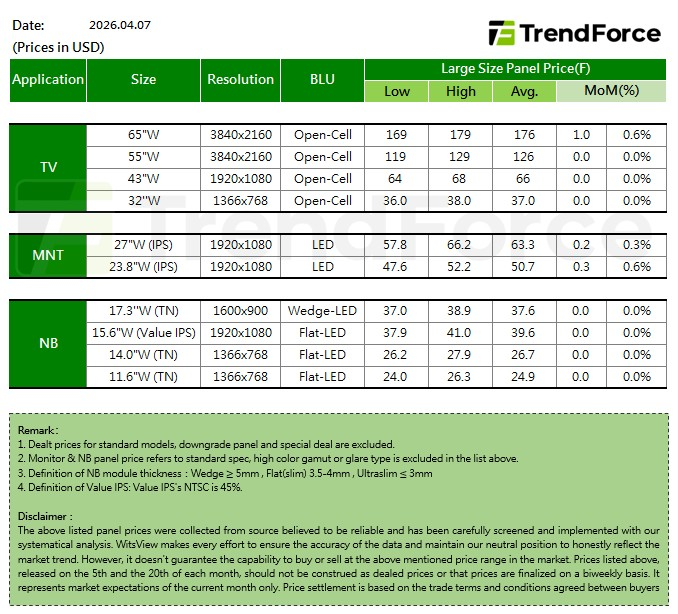

.TV

Entering April, some brands continue to maintain demand for TV panels, particularly for large-size segments. At the same time, component costs for panels have continued to rise, driven by war-related energy issues and semiconductor capacity crowding. As a result, panel makers are taking a more proactive stance on pricing, aiming to sustain upward momentum in TV panel prices in April to offset cost pressures.

However, smaller and mid-sized TV products are facing a sharp squeeze in margins due to rising memory prices. As such, it is estimated that only large-size TV panels may continue to see price increases this month, while smaller sizes are likely to stabilize. By size, prices for 32-inch to 55-inch panels are expected to remain flat, while 65-inch and 75-inch panels are projected to rise by US$1.

.MNT

Entering the second quarter, demand for LCD monitor panels remains stable. While the direct impact from rising memory prices is relatively limited, the cost of key panel components continues to increase. With demand steady and cost pressures building, panel makers are seeking to widen price increases to prevent losses from expanding. April MNT price increases are projected to be at least on par with March. For open cell panels, 23.8-inch FHD IPS panels are projected to rise by US$0.3 to US$0.4, and 27-inch FHD IPS panels by US$0.2 to US$0.3. For panel modules, 23.8-inch FHD IPS panels are expected to increase by around US$0.3, and 27-inch FHD IPS panels by about US$0.2. In addition, prices for ICs used in high-end products are rising sharply. This could create further room for panel price increases starting this month.

.NB

Entering the second quarter, brand customers had already frontloaded notebook panel inventory ahead of the end of the first quarter. Alongside ongoing memory-related issues, tight CPU supply and rising prices have emerged as another bottleneck, disrupting normal shipments. As a result, brands have advanced production wherever possible to mitigate potential risks, but this may in turn lead to a gradual softening in notebook panel demand from mid- to late second quarter. At the same time, panel makers are facing rising component costs. In response, they are no longer maintaining a conservative pricing stance, instead seeking firmer price support to reduce the risk of potential losses. As such, April notebook panel prices are currently expected to stabilize across the board, as demand begins to ease while cost pressures continue to build.

- CONTACT US

- sales@ic365buy.com

- +00852-6763-0779

- Feedback

- FOLLOW US

Smart-Core Cloud International Company Limited Copyright ©2019-2026 SMC All Rights Reserved