Recent sharp price corrections across U.S. and Chinese retail memory channels have pushed DDR5 modules to the forefront of a broader sell-off, a trend further amplified by market debates surrounding Google’s TurboQuant. This development has sparked questions about whether it signals an inflection point for weakening demand.

However, the Economic Daily News, citing Taiwan-based memory manufacturers, reports that contract prices from major memory suppliers have remained fully stable, adding that there is “no need for concern.”

The report, quoting Taiwan-based memory players, points out that fluctuations in the spot market take time to filter through to actual shipments, typically with a one- to two-month lag. As such, the recent declines in retail pricing largely reflect softer consumer demand momentum, rather than a definitive reversal in overall market demand.

Sources cited in the report note that original equipment manufacturers (OEMs) continue to rein in DDR4 production capacity, tightening market supply. Meanwhile, near-term demand remains relatively resilient—particularly in sectors such as industrial control, where substitution options are limited. As a result, Taiwan-based module makers are generally maintaining strict pricing discipline, the report adds.

DDR5 Prices Fall Sharply Across the U.S., China and Europe

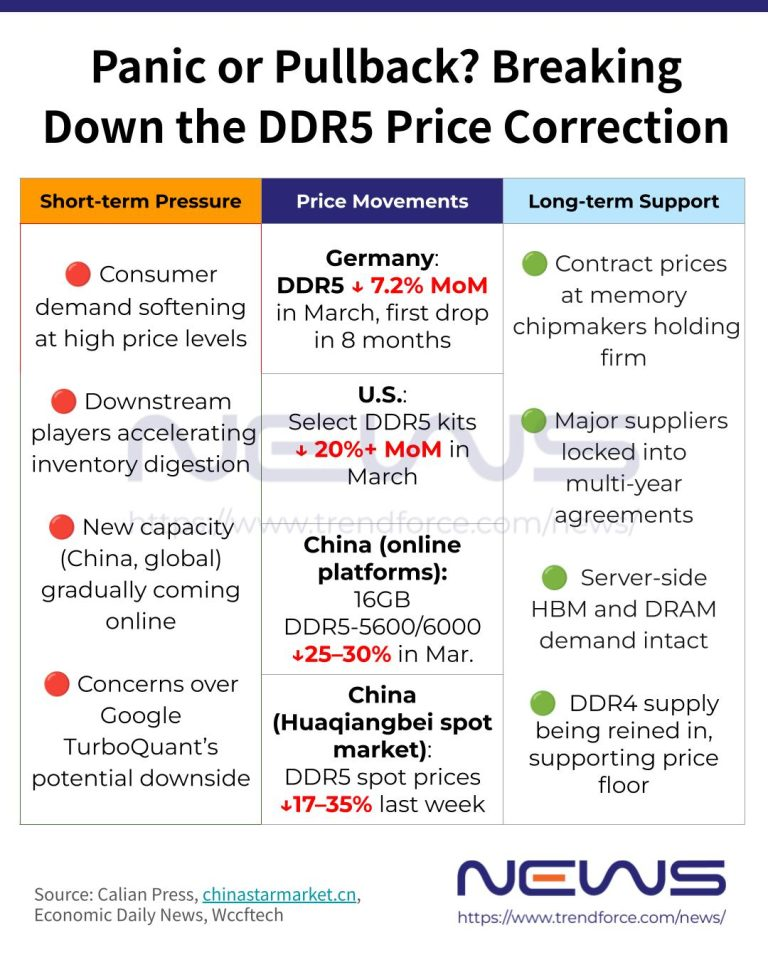

The ongoing debate appears to stem from recent price corrections in the global retail memory market. In mid-March, Wccftech, citing 3D Center, reported that DDR5 retail prices in Germany fell 7.2% month-on-month in March 2026, marking the first monthly decline following eight consecutive months of gains. Nevertheless, the report noted that the average DDR5 price remained approximately 408% higher than its level in July 2025.

This trend has since been echoed in both the U.S. and Chinese retail markets. Wccftech notes that DDR5 pricing has started to soften across major U.S. retail channels. In particular, the report highlights Corsair’s VENGEANCE 32GB DDR5 kit, which has dropped to around $379.99—more than 20% below its recent peak of $490.

Meanwhile, China’s retail market is also exhibiting a similar downward trend. According to a March 30 report from chinastarmarket.cn, prices for mainstream 16GB DDR5-5600/6000 modules on local e-commerce platforms have fallen from a peak of around RMB 1,300 in January–February to roughly RMB 1,000, representing a cumulative decline of 25%–30%.

At the same time, mainstream 32GB kits have eased from about RMB 3,800 to around RMB 3,200, with some domestic-brand products even dropping below the RMB 3,000 mark, the report notes.

Calian Press also reports sharp declines in spot prices at Shenzhen’s Huaqiangbei Electronics Market, a major electronics trading hub in China:

A 32GB DDR5 module priced near RMB 3,000 last week has since fallen by RMB 500–1,050, with some traders clearing inventory at around RMB 2,500 per unit. In more extreme cases, fire-sale prices have dropped as low as RMB 1,950.

Behind the Recent Price Correction

Notably, the current correction is largely concentrated in the consumer and retail markets. A senior executive from a listed module company, cited by Calian Press, stated that the ongoing sell-off is likely associated with softer near-term PC build demand and downstream players accelerating inventory digestion. However, he emphasized that the pullback does not alter the broader uptrend in the memory cycle, including for DRAM modules.

Chinastarmarket.cn, citing Bai Wenxi, Vice Chairman of the China Enterprise Capital Alliance and Chief Economist for China, notes that memory prices surged more than 300% from the second half of 2025 to early 2026, triggering a wave of aggressive stockpiling. Looking ahead, he expects the structural supply-demand imbalance to gradually ease, with DDR5 16GB module prices potentially normalizing by the end of 2026.

On balance, the current DDR5 price correction appears to be a consumer-driven, short-term adjustment rather than a definitive signal of structural demand deterioration. Contract prices have remained firm so far, and server-side HBM and DRAM demand has remained largely intact, with major suppliers reportedly locked into multi-year agreements with key clients. For now, the industry’s long-term fundamentals appear largely unchanged—but whether the recent turbulence proves to be a healthy market cool-down or an early warning sign may only become clear in the months ahead.

- CONTACT US

- sales@ic365buy.com

- +00852-6763-0779

- Feedback

- FOLLOW US

Smart-Core Cloud International Company Limited Copyright ©2019-2026 SMC All Rights Reserved